Building & Career

How to know you have product-market fit

A three-time founder who prices private companies for a living on why product-market fit is not a feeling but the single largest and most measurable input into what your company is worth.

I have done both sides of product-market fit. As a founder I have pushed a product at a market and prayed it would take. As a corporate-development operator and investor I have priced more than 1,000 private companies and worked deals up to roughly $26 billion, which means I have had to put an actual number on whether a company has fit or only thinks it does. So let me be blunt about the thing every deck claims and almost none can prove. PMF is not a feeling. It is the single largest and most measurable input into what your company is worth. Get it and value compounds. Fake it and you have built a machine for converting capital into nothing.

What product-market fit actually is

Marc Andreessen coined the term in 2007 and defined it cleanly: being in a good market with a product that can satisfy that market. The mechanism is the part founders skip. In a great market, he wrote, the market pulls product out of the startup. That word, pulls, is the whole game. Before fit you push: cold emails, discounts to close, every unit of growth manufactured by hand. After fit the direction of force reverses, and demand pulls the product out of you faster than you can ship it. Emmett Shear put it as the moment you stop pushing a boulder and start chasing it. Andreessen's own description of life with fit is almost embarrassingly physical: customers buying as fast as you can make it, usage growing as fast as you can add servers, money piling up in the checking account. Without fit the symptoms are equally clear: word of mouth does not spread, usage is flat, the sales cycle drags. You can feel the difference. The point of this essay is that you do not have to rely on feeling it.

How to measure it, with what fit and no-fit look like

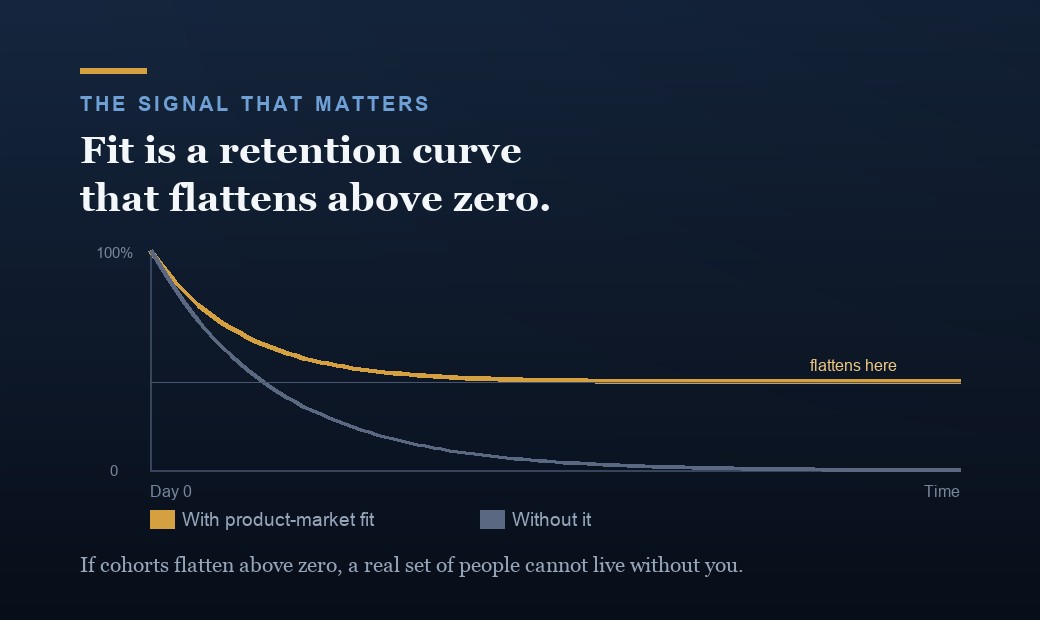

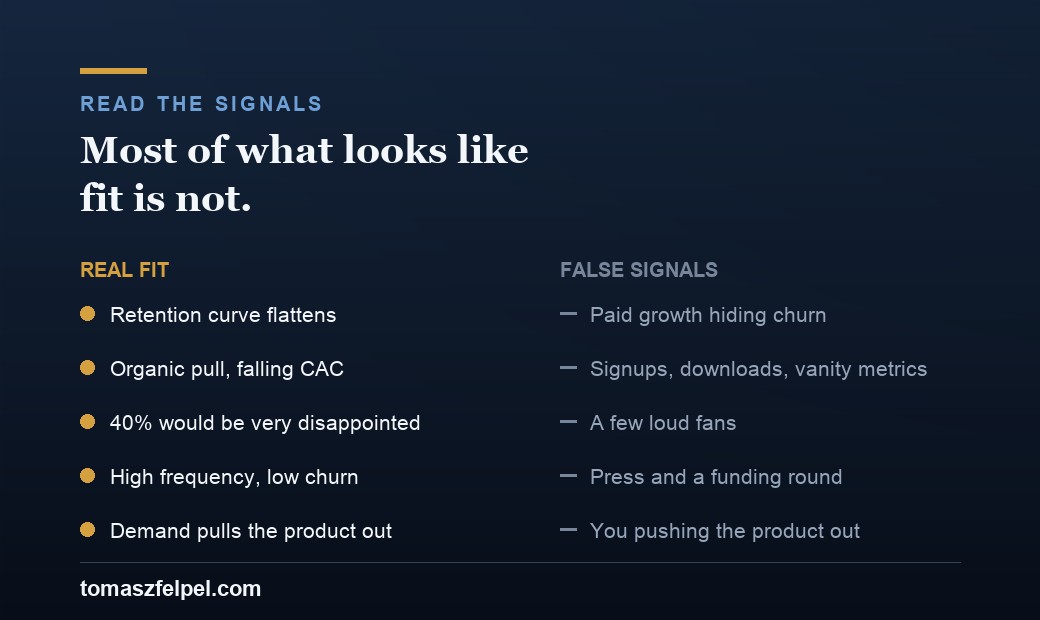

The truest objective signal is the cohort retention curve. Plot the percentage of each signup cohort still active over time. No fit is a curve that keeps sliding toward zero: everyone eventually leaves, and you are running a leaky bucket no amount of top-of-funnel will fill. Fit is a curve that declines and then flattens above zero. A stable core keeps coming back on its own. Brian Balfour says it plainly: if it flattens, you have probably found fit, at least for that segment. Andrew Chen's companion thresholds are usable today: a power-user curve that smiles, with a dense core of highly engaged users to grow out from, and actives over registered above 25%.

The fastest read is the Sean Ellis test. Survey people who have actually used the core product recently and ask how they would feel if they could no longer use it. If 40% or more say very disappointed, you likely have fit. Below that, you likely do not. Ellis did not theorize the 40% line. He benchmarked roughly 100-plus startups and found virtually none below it ever reached meaningful traction. Above 40%, growth comes relatively easily on word of mouth. Between 25% and 40% it is possible but expensive and effortful. Below 25%, companies mostly fail to grow at all.

Then watch where growth comes from. With fit, the market does your selling: a healthy benchmark is more than 50% of new accounts arriving organic or direct rather than paid, and CAC stays flat or falls as you scale. Without fit, growth is entirely bought and CAC climbs the moment you push harder. David Sacks's burn multiple, net burn divided by net new ARR, captures the same truth in cash. Pre-fit companies run 2x to 3x. Efficient post-fit growth trends toward 1.0 or below, because the market is pulling rather than your capital pushing.

In B2B and SaaS, fit shows up in the financials as net revenue retention. Best-in-class NRR runs above 130%, good is roughly 110% to 120%, and the venture-backed median sits around 106%. NRR below 100% for two or more quarters is almost always a fit problem wearing a pricing costume. Pair it with gross retention, because 100% NRR can hide 20% churn offset by 20% expansion, and best-in-class gross retention is 90% to 95%. One last signal Andreessen named in 2007: sales-cycle length, with B2B sales cycles typically measured in months, not weeks. When buyers have real intent, cycles compress and win rates rise. Deals that drag are telling you the pull is not there.

The false signals founders mistake for fit

The dominant failure mode is not absence of fit. It is the false positive. Meta's Alex Schultz says the number one problem he sees is startups that do not actually have product-market fit when they think they do. Here is what fools people. Vanity metrics: signups, downloads, page views. None survive the retention curve, which is exactly why retention is the honest one. Paid growth dressed as demand: if every new user has a CAC attached, you bought a market rather than fit it, and the bill compounds. A few loud fans: ten people who love you are a fan club, not a market, and they will not segment into a flattening cohort. Press and a launch spike: a TechCrunch bump is borrowed attention that decays in a week. NPS as proof: Andy Rachleff suggests an NPS above 40 means you are on the right track, but warns it is nowhere near as accurate as market feedback in the form of actual purchases. And the most dangerous of all: a funding round. A term sheet prices a story about your future. It is not evidence of fit. It is often evidence that you sold the story well, which is a different and more fragile skill.

Why scaling before fit is the most expensive mistake

This is where my valuation lens gets unsentimental, because premature scaling is the single most common way high-growth startups die. The Startup Genome study of more than 3,200 high-growth internet companies found that about 70% scaled prematurely, and that 74% of high-growth internet startups fail because of it. Premature scaling means one dimension, hiring, customer acquisition, or product, races ahead of the fit you have actually proven. The ceiling it creates is brutal. No prematurely-scaled startup in that dataset ever passed 100,000 users, 93% never broke $100,000 in monthly revenue, and companies that scaled in step with fit grew about 20 times faster than those that scaled ahead of it. Balfour's Four Fits explains why fit alone is necessary but not sufficient: to reach $100 million you need market-product, product-channel, channel-model, and model-market fit interlocking as one system. Pour fuel on a product before those locks click and you do not accelerate. You set the money on fire faster.

Fit is a moving target that erodes

Even real fit is not a trophy. It is a position you hold against a market that keeps moving. Rahul Vohra's Superhuman is the cleanest proof that fit is a measurable, improvable score rather than a binary state. They started at 22% very-disappointed in 2017, below the bar. By focusing on high-expectation customers the number rose to 33%, and after about three quarters of disciplined work it hit 58%. The method matters: segment to the users who would be very disappointed, learn precisely why they love it, mine the somewhat-disappointed fence-sitters whose needs align with your core benefit, ignore the not-disappointed, and split the roadmap roughly 50/50 between deepening what users love and removing the friction blocking the fence-sitters. Then resurvey, every quarter, forever. Competitors copy you, buyer expectations rise, your best segment matures, and the score you earned last year decays if you stop running the engine. Treat fit as a metric you maintain, not a milestone you pass.

How investors and acquirers price the difference

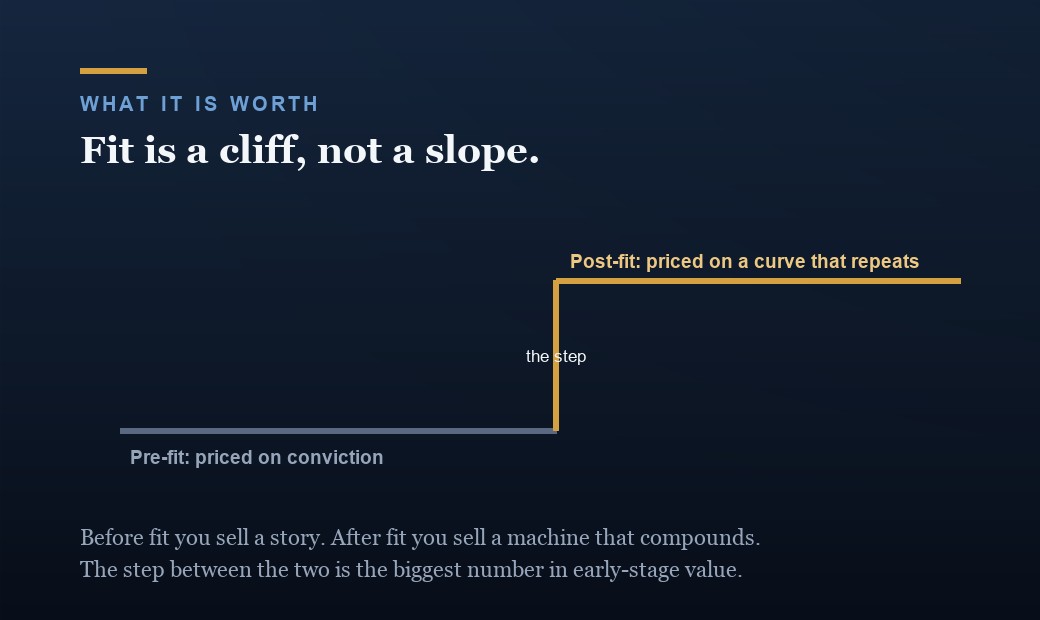

Now the part I get paid to know. There is a value cliff between pre-fit and post-fit, wider than founders expect, because fit changes what a buyer is actually purchasing. Before fit, an acquirer or investor is buying a hypothesis: a team, some technology, a story about a market. They discount it heavily because most hypotheses are wrong. After fit, they are buying a demonstrated cash-generating engine: retention that flattens, NRR above 110%, organic pull, a falling burn multiple. Those are not adjectives. They are durable, forecastable numbers, and forecastable cash is what carries a premium multiple. Revenue compounding off a 130% NRR base is worth multiples more than revenue leaking through 90% NRR, because one grows without new spend and the other needs constant refueling. And here is the trap the Genome data exposes. Before the scale stage, prematurely-scaled startups are valued at roughly 2x as much and raise about 3x more money than the disciplined ones. That premium is a loan against fit you have not proven, and the market calls it in at the worst possible time, when your cost structure is built for a demand curve that was never real.

What it is worth, from someone who has to put a number on it

If you take one thing from a person who prices this for a living: do not let a fundraise convince you that you have what the retention curve says you do not. Capital is the easiest fit signal to fake and the most expensive to be wrong about. Open your cohort chart and ask whether it flattens above zero. Run the Sean Ellis survey and read the 40% line honestly. Check whether more than half your new accounts arrive without paid help. Look at your NRR over the last two quarters, not your best one. If those numbers are there, you have the single largest driver of enterprise value, and your job is to protect it and scale into it deliberately. If they are not, no round, no logo wall, and no press hit will manufacture them, and the kindest thing you can do is keep pushing the boulder until the day the market reaches back and starts pulling. You will not have to wonder when that happens. You will be able to measure it.

Common questions

How do you measure product-market fit instead of guessing at it?

Start with the cohort retention curve. If it flattens above zero, a stable core keeps coming back and you likely have fit. Then run the Sean Ellis survey: 40% or more saying they would be very disappointed without your product is the bar. Add organic acquisition above 50% of new accounts, a burn multiple trending toward 1.0, and net revenue retention above 110%. Those are numbers, not vibes.

What is the 40% rule for product-market fit?

Sean Ellis survey recent users with one question: how would you feel if you could no longer use this product. If 40% or more say very disappointed, you likely have fit. Below that you likely do not. Ellis did not invent the number. He benchmarked roughly 100-plus startups and found virtually none below 40% ever reached meaningful traction. Above 40%, growth comes relatively easily on word of mouth.

What do founders mistake for product-market fit?

Almost everything that feels good. Signups and downloads are vanity metrics that the retention curve quietly kills. Paid growth is a bought market, not a fit one, and the bill compounds. A handful of loud fans is a fan club, not a market. A press spike is borrowed attention that decays in a week. The most dangerous false signal is a funding round. A term sheet prices a story, not proof that demand pulls your product out of you.

Why is scaling before product-market fit so expensive?

Because it caps the company and then breaks it. In the Startup Genome data of more than 3,200 high-growth startups, about 70% scaled prematurely and 74% failed for that reason. No prematurely-scaled startup ever passed 100,000 users, and 93% never broke $100,000 in monthly revenue. You build a cost structure for a demand curve that was never real, then the market calls the loan at the worst possible time.

How much more is a startup worth after product-market fit?

There is a real value cliff. Before fit, an investor or acquirer is buying a hypothesis they discount heavily because most hypotheses are wrong. After fit, they are buying a demonstrated cash engine: flattening retention, NRR above 110%, organic pull, a falling burn multiple. Forecastable cash carries a premium multiple. Revenue compounding off a 130% NRR base is worth multiples more than revenue leaking through 90% NRR, because one grows without new spend.

Related reading

- How to value a pre-revenue startup, when there is no revenue to discount.

- What acquirers really pay for, and the line items they quietly discount.

- The cofounder is the most expensive line on your cap table.

- Building without warm intros: why the outsider's rigor became my edge.

Go deeper

If you are trying to read your own retention curve honestly, or staring at a fundraise you are not sure your fit can support, let's work the actual numbers together, or read more of how I think about it.

Tomasz Felpel is an investor, founder, and advisor in private markets and healthcare, based in New York. He is a three-time founder of Value Alpha, an AI-powered private-markets valuation platform, Sonnerie VC, an early-stage healthcare venture firm, and Pond. Previously he led corporate development and M&A at Fortune 500 scale, pricing more than 1,000 private companies. Columbia Business School EMBA. Read the full story.